Mutual Funds vs ETFs

Mutual Funds and ETFs (Exchange-Traded Funds) are both investment vehicles. In some cases, they may follow the same index or hold the same stocks and seem interchangeable. However, mutual funds and ETFs have 2 key differences.

- Trading: ETFs trade like stocks (instantaneously). You buy shares at their current price. Mutual funds orders are processed only at the end of the day, and purchases are based in dollars, not shares.

- Tax Efficiency: Mutual fund investors pay capital gains tax on assets sold by their funds (even if you don’t sell). ETF owners pay capital gains tax only when they sell their shares.

Takeaway: In retirement accounts (401(k), 457, or Roth IRA) where capital gains are not relevant, mutual funds and ETFs are very similar. However, in a taxable brokerage account a mutual fund may be subject to capital gains earlier than an ETF. This tax drag generally makes ETFs preferable in taxable brokerage accounts.

Stay the Course

Stay the course! Many investors get spooked when the stock market drops suddenly. It’s understandable. There’s a natural urge to sell, sit on the sidelines, and then re-invest when the outlook is brighter. However, research studies have shown that investors do much better when they “stay the course”. In fact, market drops can be beneficial for investors. Shouldn’t you want stock prices to be lower when you’re buying them (working years), and want stock prices to be higher when you’re selling them (retirement)? Many working investors see market drops as an opportunity to buy stocks “on sale”.

Not convinced and still think selling after a market drop is a good idea? Consider that January 2002 – January 2022, 7 of the 10 best stock market days occurred within 15 days of the 10 worst days. Those who sell after big drops are likely to miss big gains. Selling low and buying high is not a great investing strategy. Stay the course!

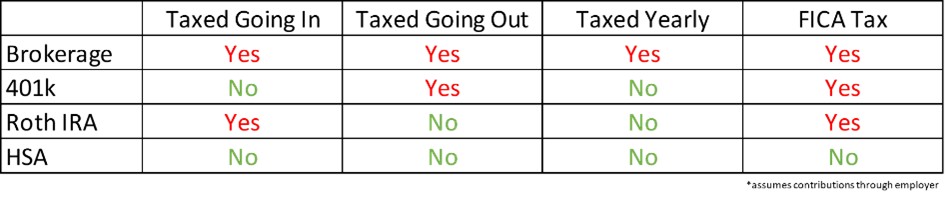

Tax Profile of Investment Accounts

Investment returns are strongly influenced by taxes. It’s important to know the tax treatment of investment accounts to optimize asset location, minimize your tax bill, and maximize your purchasing power.

Brokerage accounts are not tax advantaged accounts. They get no special tax treatment. Money invested in brokerage accounts is subject to immediate income and payroll taxes in addition to capital gains and yearly ordinary income on dividends. 401(k) pre-tax accounts and Roth IRAs are both tax advantaged but differ when income taxes are paid. The Health Savings Account (HSA) is the most tax-advantaged account and can potentially avoid all taxation leading to the highest returns of all the accounts. This is why it’s generally recommended to fully fund an HSA before these other accounts.

Direct Index Investing

Direct index investing is a newer investment approach that involves owning individual stocks or bonds directly, rather than through a mutual fund or exchange-traded fund (ETF). The main advantage is an increased ability to utilize tax loss harvesting. However, direct index investing has several disadvantages.

- The strategy creates lots of complexity, requiring significant time (aka cost) in properly maintaining the strategy. This may be worthwhile for multi-million-dollar taxable portfolios, but not for most American families.

- Most investors have most of their assets in tax-advantaged accounts (401(k), 457, Roth IRA, 529, HSA, etc.). Direct index investing provides no benefit in these accounts.

Direct index investing does not seem to be a good strategy for most everyday investors. If you’d like a second opinion on this strategy or another advanced investment strategy, many fiduciary financial advisors offer free meetings.

Your Money or Your Life

“Your Money or Your Life” by Vicki Robin and Joe Dominguez is a time-tested classic for those interested in FI (financial independence) or FIRE (financial independence, retire early). It’s a guide that addresses money issues head-on to avoid autopilot behaviors and ensure you make thoughtful, intentional decisions regarding money. This book is about creating a strategy to design money behaviors to create your ideal life.

If you struggle with saving, feel that money just disappears or want to work towards future goals more efficiently, this book can provide awareness and be the wakeup call that helps align your usage of money with your values.

Types of Financial Advisors

Financial Advisors are not a homogeneous group. There are dramatic differences in what some advisors do and the value they provide.

- Financial planners: focus on financial advice. They develop a plan for you to live your best life and take full advantage of your unique financial opportunities. May charge a fraction of assets under management (AUM), a flat-fee, or hourly. May or may not directly manage your investments.

- Investment managers: focus on managing your investment portfolio. Typically charge AUM. Robo-advisors can provide a similar service, typically at a much lower price.

- Financial salesmen: focus on selling commissioned products including investments, whole life insurance, annuities, etc.

Families typically benefit most from working with financial planners. Financial planners optimize your entire financial picture, and many have a fiduciary requirement to put the client’s interests above their own interests.

It’s important to understand how financial advisors are paid and what conflicts of interest they may have. Terms like fiduciary, fee-only, fee-based, advice-only can be helpful in finding an objective and transparent financial advisor. If you find this industry confusing, you’re not alone. Asking clarifying questions is encouraged. A good financial advisor should always be transparent and take time to address your questions and concerns.

Medicaid

Medicaid is a government-funded healthcare program in the United States designed to assist low-income individuals and families with medical costs. Medicaid covers a range of medical services, including doctor visits, hospital care, prescription drugs, and long-term care. Eligibility and benefits vary by state.

Most think of Medicaid as only helping the poor, but it also becomes an important consideration for end-of-life planning. Medicaid can effectively serve as a “backstop” which allows you to have more confidence in spending down assets. Medicaid can step in if you live much longer than expected or incur significant medical expenses late in life. Medicaid will not force you to sell a primary home or primary car but may seek reimbursement from these assets after you pass.

Stock Options

Stock options are a common form of employee compensation, often targeting higher level employees. Stock options give employees the right (but not obligation) to purchase company stock in the future at a predetermined price, known as the “strike” or “exercise” price. If the company’s stock price increases, this may be very valuable. If the company’s stock price decreases, stock options may be worthless.

Options may have a vesting schedule, meaning you need to work for a specific period to be eligible to exercise them. After vesting, you can exercise the options by buying the stock at the exercise price, despite the current market price. Stock options typically have an expiration date, so you must exercise them before this date, or they expire. Taxation depends on the type of stock option.

Employees with stock options should consider portfolio risks associated with a concentrated position in a single company.

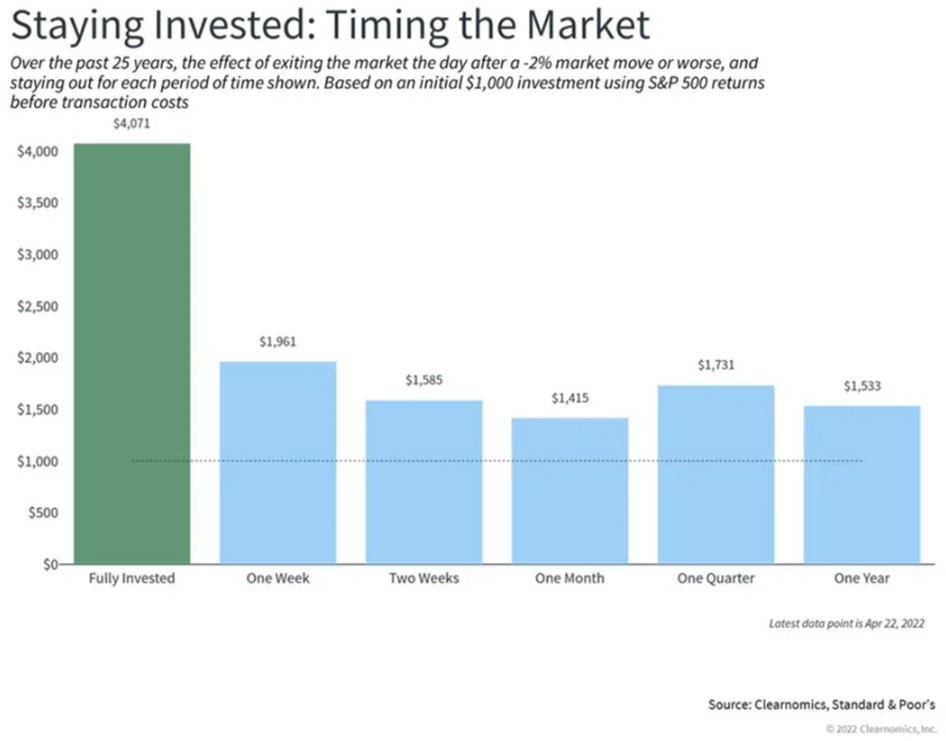

Staying Invested vs Timing the Market

When the stock market has a big drop, it’s natural to consider selling and waiting in cash until the market bottoms out, but that’s generally a very bad idea. Investors are usually best suited by staying fully invested.

S&P 500

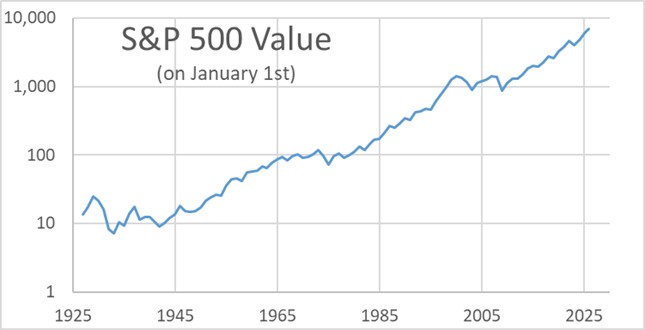

The S&P 500 is a stock market index that tracks the 500 largest publicly traded companies in the United States. These 500 companies comprise about 80% of the market value of all US publicly traded companies, making the S&P 500 a common measure for the overall performance of the US stock market.

The S&P 500 is market capitalization weighted. This ensures the S&P 500 better tracks movements of the stock market than price weighted indexes like the Dow Jones Industrial Average.

Inherited Investment Accounts

Inherited investment accounts are treated differently under the federal tax code.

- IRAs/401(k) – these pre-tax accounts have not yet been taxed. Withdrawals by the beneficiary will be treated as taxable income.

- Roth IRAs – these post-tax accounts can be withdrawn tax-free by the heir.

- Taxable accounts – these accounts receive a basis “step-up” to the current value upon the decedent’s death. This potentially reduces capital gains tax when withdrawn.

Generally, a non-spouse must liquidate inherited retirement accounts within 10 years of the decedent’s death. This can create adverse tax issues, especially for pre-tax accounts. Some estate planning strategies may prioritize taxable accounts for inheritance to avoid withdrawal rules and avoid potentially significant capital gains.

Active Investing Underperformance

Want to outperform the stock market? Good luck. According to SPIVA’s Scorecard, only 27% of active large cap funds outperformed the S&P 500 over a 12-month period and only 12% outperformed over a 10-year period (risk-adjusted returns, ending June 30, 2025). Generally, the longer the time period, the more unlikely an active fund will outperform the market.

But why? It generally comes down to fees and the efficiency of the market. Basically, even experts don’t know what’s going to happen in the future. Data show they can’t consistently pick the winners. Their performance is essentially random. The fees on an active fund act as a drag on the investor’s performance. The higher the fees, the less likely to outperform the market. This is why an increasing number of investors are ditching active investments for index funds.

457 Plans

A 457 plan is like the well-known 401(k) plan but has key differences. Both are tax-advantaged retirement savings plans allowing an annual contribution limit of $24,500 in 2026. Those aged 50 and over can also contribute an additional $8,000 as a “catch-up” contribution and may be eligible for “special catch-up” contributions. Contributions to both plans are tax-deferred, reducing your taxable income in the year you contribute.

457s differ from 401(k)s in that 457s are available to government and certain non-profit employees, while 401(k)s are for the private sector. Unlike 401(k)s, 457s are not governed by ERISA and have no penalties for accessing funds before age 59 ½. 457 plans also have a unique 3-year catch-up provision. Employee deferral contributions to 457s are separate and not combined with other deferral contributions retirement plans such as 401(k)s, 403(b), etc. These unique features can make 457s valuable, especially for high savers and early retirees.

What is an Index Fund?

Index funds are investment vehicles that aim to replicate the performance of a specific market index, such as the S&P 500. They offer a passive and cost-effective way to invest in a broad range of assets, like stocks or bonds. Index funds can provide diversification and align with a disciplined, data-driven approach to investing. This can help minimize the behavior gap and achieve long-term financial goals.

Index funds can provide several advantages: diversification, low costs, transparency, consistency, tax efficiency, simplicity, etc.

Time Value of Money

$100 is $100, but $100 today is not the same as $100 in 1950. Modern economies are designed for low level inflation. The U.S. Federal Reserve targets 2% inflation. When thinking about costs, you may want to consider the Consumer Price Index (CPI) Inflation.

Investments generally grow faster than inflation, leading to wealth accumulation. US Stocks compounded nearly 10%/yr from 1928-2025. When thinking about investments you may want to consider the historical returns of various indexes. Understanding the time value of money can help you achieve your financial goals.

Why Does the Stock Market Grow?

Why does the stock market grow? The stock market grows because most companies are profitable, and the U.S. economy grows. Failing companies are replaced by new, profitable companies. In a simplified world, the P/E ratio would be constant. In other words, the Price of a stock would be a multiple of company Earnings. As company earnings continue to increase due to growth and inflation, so should stock prices and the stock market. Valuations are almost always plotted on a linear scale but are better understood on a log scale. The last 100 years show steady long-term growth.

Capital Gains and Basis

Capital gains refer to the profit earned from selling an asset like stocks. Basis is the original cost of the asset. The capital gain is calculated by subtracting the basis from the selling price. When you sell stock in a taxable (brokerage) account, you don’t pay tax on the total transaction value, just capital gains (aka profit). To encourage investing, capital gains tax rates are lower than marginal tax rates.

Mega Backdoor Roth IRA

A Mega Backdoor Roth IRA is an advanced retirement savings strategy that goes beyond the Backdoor Roth IRA strategy. It involves making after-tax contributions to a 401(k) plan then converting those contributions to a Roth IRA or Roth 401(k). This circumvents both income restrictions and maximum contribution limits of other Roth funding strategies. Due to the complexity, consulting a financial planner or accountant may be wise.

The Mega Backdoor Roth IRA strategy can allow one to fund a Roth IRA to a high level in a short period of time, but there are rules. Although after-tax contributions to the 401(k) do not count against the $24,500 pre-tax limitation (2026), they still apply to the $72,000 total 401(k) contribution limit. In addition, whether to allow this transaction and how frequently it can be transferred to Roth will be dictated by the specific 401(k) plan. Your company’s plan is unlikely to mention “mega backdoor” but may refer to in-plan Roth conversions.

Dow’s 401(k) plan does allow this Mega Backdoor Roth IRA strategy.

Backdoor Roth IRA

A Backdoor Roth IRA is a strategy that allows individuals to contribute to a Roth IRA even if their income exceeds the direct contribution limits (phaseouts begin at $153k single, $242k married filing jointly in 2026). This method involves making a non-deductible contribution to a Traditional IRA and then converting it into a Roth IRA. It seems like a workaround of the income limitation rule, and it is. However, the IRS considers it allowable, and the maneuver has been “blessed” by Congress in the 2017 Tax Cuts and Jobs Act.

However, one should be careful with this maneuver and consider consulting a financial planner or accountant. If one has a Traditional IRA, the “pro-rata” rule will apply, and the maneuver would create a taxable event. The pro-rata rule states that when a Traditional IRA contains both non-deductible after-tax funds and deductible pre-tax funds, each dollar withdrawn from the IRA will contain a percentage of tax-free and taxable funds relative to the proportion those funds that make up the account. One can’t convert only the non-deductible portion that doesn’t trigger a taxable event.

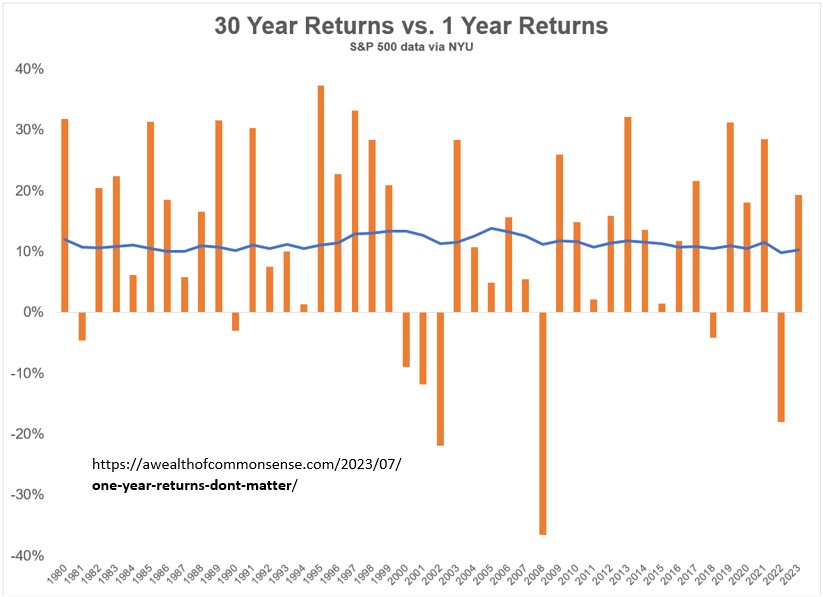

Investing Timeframe

What is your investing timeframe? If you’re planning for retirement, your timeframe isn’t the time until retirement. You’ll likely remain invested throughout retirement until your long life finally concludes. This could be 60+ years for younger investors and even 30+ years for many retirees.

Retirement planning should focus on reliable long-term trends, not today’s daily news or even last year’s returns. One-year returns make a minimum impact on most investors’ long-term plans. No need to stress out. If you focus on long-term planning, you should be just fine.

Health Savings Accounts (Tax Savings)

A health savings account is quadruple tax-free: 1) no taxes on contributions, 2) no taxes on withdrawals, 3) no taxes on earnings, 4) no FICA taxes if provided through an employer.

HSAs can also act as a super-charged retirement account. Many pay medical expenses out of pocket and let this advantaged account grow. HSAs can be accessed in retirement based on medical expenses incurred throughout your lifetime. Save receipts or EOBs. HSA reimbursements do not have to be the same year as the expense. Generally, HSAs should be funded before Roth IRAs and 401(k)s beyond the employer match due to the advantaged tax benefits.

Comprehensive Financial Planning

Comprehensive financial planning can vary dramatically among financial planners/advisors. However, true comprehensive financial planning covers all financial aspects of your life. It provides a roadmap to your consciously selected best future life based on your personal values. It provides a deep dive to eliminate blind spots, ensure you’re investing efficiently, minimize lifetime taxes, and properly address potentially damaging risks. It optimizes your financial outlook to make reaching your goals as easy as possible.

Comprehensive financial planning generally refers to an ongoing relationship including regularly scheduled meetings exploring numerous topics with a financial planner. This model is typically appropriate for those who want to maintain a relationship and have the advisor maintain the lead role. For those who prefer a more self-reliant approach, a one-time financial plan may be more appealing.

Trading Time of Mutual Funds and Stocks

The trading time of mutual funds and stocks/ETFs differs. Stocks and exchange traded funds (ETFs) trade throughout the day so buy/sell orders are processed immediately. However, mutual funds trade only once per day, typically after the market closes. Investors can place a buy/sell order at any time during the day, but that transaction will not be processed until the market closes, at the closing price. All transactions for a mutual fund are processed together.

Due to these differences, stocks are usually purchased on a shares basis (buy 1 share of Stock ABC), while mutual funds are usually purchased on a dollars basis (buy $100 of mutual fund XYZ).

What is AUM?

What is AUM? AUM is an acronym for assets under management. AUM is a traditional billing method for investment management. It does not define the services provided.

Before the widespread usage of personal computers and the internet, investors used phones to call stockbrokers or visited brokerage offices to communicate investment decisions. It was a clunky process and there was no internet to guide an investor. Many investors chose to pay an investment manager to invest their money for them. These investors were charged a percentage of assets under management (AUM) for this service. Fees were automatically deducted from the accounts, so investors rarely noticed how much they paid.

Today it may seem silly to pay someone 1% per year to invest your money when anyone can invest it themselves (1% of $1 million is $10k/yr). Computer algorithms (aka robo advisors) can provide diversified portfolios at a fraction of traditional AUM costs. But momentum is powerful, and many investors still pay for this service.

Decades ago, investment management was much more valuable than it is today. Today the value is in financial planning. Some advisors provide financial planning but still charge based on investment management. As the industry evolves, provided value and AUM billing diverge further and further. This has led to new, more transparent billing models: flat fee, subscriptions, hourly, etc.

Options

Options are contracts that grant the holder the right, but not the obligation, to buy (call option) or sell (put option) a specific asset (like stocks, bonds or commodities) at a predetermined price (strike price) within a set period. They provide flexibility and can be used for hedging against market fluctuations or speculating on price movements.

Options are essentially a zero-sum game. Every options contract that has a winner, also has a loser. That’s not to say options are inherently bad, especially when used as protection.

Participating in options should not be confused with investing. Options are typically not appropriate for everyday investors.

Buffet vs Hedge Funds Bet

In 2007, Warren Buffet challenged the entire hedge fund industry to a bet: $1 million whether a selected hedge fund would outperform the S&P 500 over the next 10 years. Eventually someone accepted Buffet’s bet and chose 5 funds investing in hedge funds. It wasn’t even close. Hedge funds rarely outperform passive investing.

Traditional IRAs

Traditional IRAs (Individual Retirement Accounts) are tax-advantaged investment accounts commonly used for retirement savings. They allow contributions to avoid current year taxation and to grow tax-deferred until withdrawal.

Traditional IRAs are most commonly used to rollover funds from a previous employer’s retirement plan. However, IRAs are also useful accounts for employees without an employer sponsored retirement, those wishing to contribute tax-deferred on behalf of a non-working spouse, or those utilizing backdoor Roth IRA strategies due to high income.

These accounts are easy to establish. It’s important to be aware of contribution limits, eligibility criteria, and potential tax implications.

Lump Sum Investing vs Dollar Cost Averaging

Investors seeking to invest significant sums of money (from a work bonus, inheritance, etc.) often wonder about whether to invest it all immediately (lump sum investing) or spread the investment over time (dollar cost averaging). Lump sum investing typically results in higher returns, but it’s riskier. This is because the market is usually moving upwards, so the earlier money is invested, the better. Dollar cost averaging reduces short-term risk by spreading investments but may miss out on immediate market gains.

There’s no right or wrong decision as long as you make an informed decision. Some prefer the path that’s more likely to result in the higher balance. Some prefer the path that’s likely to limit regret if the market drops substantially. It’s not about the best choice. It’s about your best choice.

An independent financial advisor can advise on your entire portfolio (rather than managed assets) to ensure your portfolio is tax efficient.

How to Build a Portfolio

What does a good investment portfolio look like? A good investment portfolio should be diversified, low fee, risk appropriate, and tax efficient.

Target date funds may be a good guide to model your investment portfolio. Target date funds were designed as a single investment appropriate for a typical investor based on age. Not surprisingly target date funds developed by the major brokers look very similar to each other. They typically are very diversified, have low fees, and appropriate risks.

Note that target date funds are not particularly tax efficient. This can be overcome through asset location. The entire portfolio may look like a target date fund, but stocks and bonds are shifted to accounts which provide the best tax efficiency.

An independent financial advisor can advise on your entire portfolio (rather than managed assets) to ensure your portfolio is tax efficient.

Value of a High Deductible Health Plan

High deductible health plans (HDHPs) can be a cost-effective choice for many individuals and families. Compared to traditional health plans, HDHPs have lower premiums but higher deductibles. In comparing these plan options it’s important to distinguish key terms.

- Premiums must be paid regardless of health care usage.

- Deductibles are the amount you must pay out of pocket for medical expenses before insurance coverage kicks in.

- Max out-of-pocket is the maximum amount you would pay in a single year before the insurer covers 100% of expenses. Deductibles, but not premiums, are included in the max out-of-pocket.

Health plans can vary dramatically, but generally a HDHP will be much more attractive in years with minimal health care (save on premiums) and years with extensive health care (less paid to reach max out-of-pocket). Sometimes HDHPs are also more attractive in moderate health care usage scenarios, making them always cheaper than low-deductible plans with the same medical coverage.

Those enrolled in HDHPs are eligible to contribute to a health savings account (HSA). This is a huge deal since HSAs are completely tax-free, typically reducing taxes by several thousand dollars per year. If you’re not in a high deductible health plan with an HSA, you should strongly consider enrolling next year. HDHPs are often a much better option.

401(k)s

A 401(k) is a retirement savings plan offered by many employers. It allows employees to contribute a portion of their salary to a tax-advantaged account. In many cases the employer will also contribute to the employee’s account. In 2025, the annual contribution limit is $23,500. Those aged 50 and over can contribute an additional $7,500 as a “catch-up” contribution. Under a change made in SECURE 2.0, employees aged 60, 61, 62, or 63 have a higher maximum catchup contribution of $11,250 instead of $7,500. Employees typically have the option to contribute on a pre-tax or post-tax basis.

Pre-tax: Contributions are tax-deductible, reducing your current taxable income. Distributions in retirement are taxed as income.

Post-tax: Contributions are not tax-deductible, so current taxable income is not reduced. Distributions in retirement are tax-free.

Pre-tax 401(k)s are the primary retirement savings accounts for most retirees.

Sunk Cost Fallacy

Behavioral finance bias refers to how psychological biases influence financial decisions. One common behavioral finance bias is sunk cost fallacy. It refers to the tendency to continue investing time, money, or resources into a project or endeavor simply because you’ve already invested a significant amount, even if it no longer makes rational sense to do so.

Consider you bought stock XYZ at $100 per share. It dropped to $50 per share. You don’t want to sell it until it returns to $100.

Now shift the framing. Are you willing to buy stock XYZ at $50 per share today? If the answer is no, and you value $50 greater than 1 share of stock XYZ, you should reconsider your decision to hold the stock. The price you paid for XYZ doesn’t impact the value today.

Bond Duration

Bond Duration is a crucial concept to understand when investing in bonds. It represents the weighted average time it takes for an investor to receive the bond’s cash flows, including both periodic interest payments and the return of the bond’s principal. Longer-duration bonds are more sensitive to changes in interest rates, meaning their prices can fluctuate more with interest rate changes. Shorter-duration bonds are less sensitive.

What is Depreciation?

Depreciation is an accounting method that allocates the cost of a tangible asset (such as a building, vehicle, or equipment) over its useful life. Depreciation reflects the gradual decrease in value of the asset due to wear and tear, obsolescence, or other factors. A depreciation expense is deducted from the company’s income, reducing taxable income. Depreciation recapture may occur if assets are sold for a higher value than the depreciated value. Depreciation is commonly encountered for individuals with rental property. It can be important in financial planning, as it impacts financial statements and taxes.

Community Property or Equitable Distribution States

State law dictates property ownership for couples. Nine states, including Texas, are community property states. Forty-one states, including Michigan, follow equitable distribution ownership.

- Community property states attempt to distribute property as close to a 50-50 split as possible. Almost all property is equally owned by a couple. It is possible to keep some assets individually owned, but care must be taken. Separate property in a community property state may include assets obtained before marriage or a received via inheritance. However, these assets must remain separate from joint property to retain their separate ownership status.

- Equitable distribution states divide property based on a determination of what’s fair under the circumstances of each case. In deciding on splitting property in a divorce a judge may consider factors such as length of the marriage, spouses’ contributions, spouses’ ages and needs, earning ability, and past conduct.

Flexible Spending Accounts

Flexible Spending Accounts (FSAs) allow pre-tax contributions to cover qualified medical or dependent care expenses. This effectively reduces the cost of covered expenses by your marginal tax rate.

FSAs have annual contribution limits and a “use it or lose it” rule but may have a grace period or carryover feature. For medical FSAs the entire yearly amount contribution is available on day one, even if you haven’t contributed yet. It’s important to plan wisely and budget for eligible expenses to maximize the benefits of these accounts. FSAs can be very useful for predictable expenses like glasses, braces, prescriptions, or child daycare.

Flexible spending accounts are sometimes confused with health savings accounts (HSAs). Both are earmarked for medical expenses but are very different. FSAs are a one-year cash account. HSAs are multiyear investment accounts. An individual can have a medical FSA or an HSA. It’s not generally permitted to have both in the same year.

Don’t Hire a Financial Advisor to Beat the Market!

Don’t hire a financial advisor to beat the market! Unfortunately, there’s no magic weight loss pill, no reliable get rich quick sales strategy, and no consistent way to beat the stock market. Attempting to beat the market is a fool’s errand which typically leads to underperforming the market. Nearly all advisors know this.

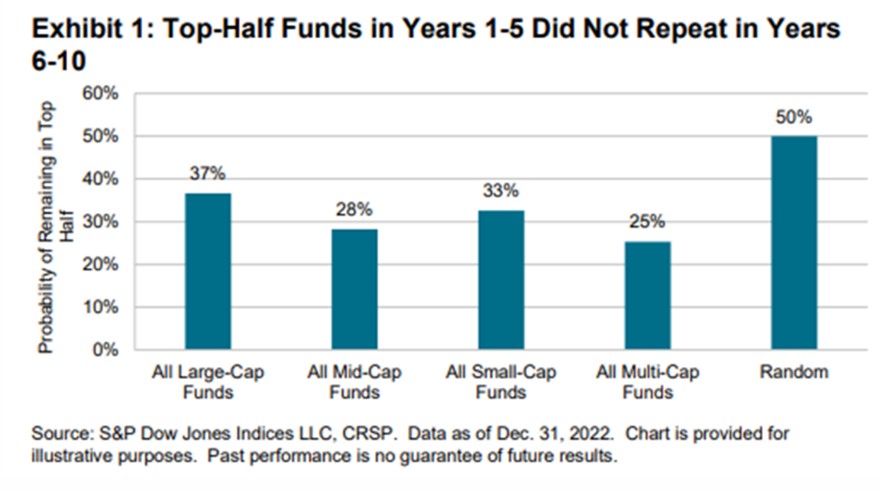

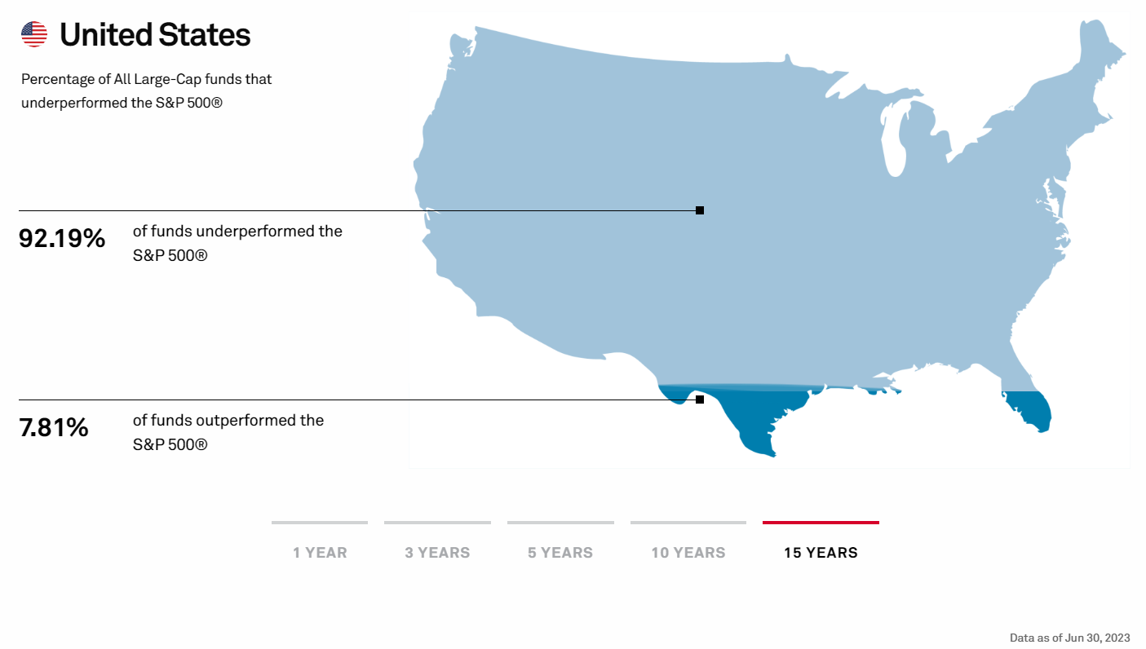

S&P Global compiles active fund management against their index benchmarks. Their 2024 report shows 89.5% of active large-cap funds underperformed the S&P 500 over the prior 15 years. But 10.5% did outperform so just choose those funds, right?

S&P Global also tracks performance over time to determine whether overperformance is due to skill or luck. Their 2024 report shows that among funds in the top half of performance for a 5-year period, they routinely performed below what random luck would suggest for the following 5-year period. Yes, randomly selected funds typically show better future performance than past “winners”. Their report sums it up well: “active outperformance, when it occurs, tends to be the result of luck rather than genuine skill.”

The correct reason to hire a financial advisor is to clarify your financial picture, identify missed opportunities, reduce taxes, and ensure you’re investing efficiently so you can reach your goals as easily as possible.

Should You Underfund a 529?

Funding a 529 College Savings Plan can be different than a 401(k).

Underfunding a 529 still allows for part-time work, scholarships, financial aid, or student loans to fill the gap. Underfunding retirement can be a big problem. There is no opportunity to borrow.

Overfunding a 529 can potentially lead to penalties if funds are not used for qualified educational expenses. Money can get trapped in these accounts. Overfunding a retirement account doesn’t have this downside. You’ll simply have more money.

Some choose to “baseload” a 529 at 60-80% of expected need and then invest the rest in other accounts with more flexibility (used for education or retirement). Some investors choose to invest more aggressively in 529s than retirement accounts due to risk differences.

Although the Secure 2.0 Act (2022) now allows for some 529 overfunding to be rolled into a Roth IRA with restrictions, investors should still be careful about overfunding 529s. Additionally, investors should consider whether their 529s should be invested differently than their retirement accounts.

Medical Power of Attorney

A Medical Power of Attorney is a legal document that allows someone to make healthcare decisions on your behalf if you become unable to do so. This granted power again becomes inactive once the individual is again able to make healthcare decisions on their own.

This document avoids potential delays and complications that could result if one needs to seek court approval to make medical decisions on behalf of another individual.

A medical power of attorney is a legal document that must be drafted by a lawyer. It’s often part of an estate documents package.

Pension Plans

Pension plans are retirement benefit plans. Their popularity has waned in recent decades, but many employees still have pension plans. Unlike a 401(k), pension plans are controlled by the employer. The employee cannot contribute and does not manage these accounts. Pension plans can be grouped into two categories.

Defined benefit plans provide participants with pre-determined formula-based benefits at retirement. The final benefit is defined by the employer.

With defined contribution plans the employer contributes funds to a tax-deferred account for an employee. The growth of the account is not pre-determined, and the final value is typically reliant on the stock/bond markets. Only the contribution is defined.

Pension plans are typically structured as an annuity for retirees (monthly payments for life). However, some pension plans offer a lump sum payout that the retiree can transfer to an individual retirement account.

Portfolio Turnover

8/5/25

Portfolio turnover is a measure of how frequently the holdings within an investment portfolio are bought and sold within a specific period, typically a year. Here’s why it matters:

- Cost Implications: Frequent trading can lead to higher transaction costs, including brokerage fees and bid-ask spreads. High portfolio turnover can erode returns over time.

- Tax Efficiency: Frequent buying and selling can generate capital gains. Low turnover strategies can be more tax efficient.

- Investment Strategy: High turnover may imply an active approach, while low turnover suggests a buy-and-hold or passive strategy.

- Risk Management: High turnover can introduce market timing risk.

For investors choosing active mutual funds or ETFs, it’s important to consider portfolio turnover. Passive funds often have very low portfolio turnover due to their design.

The Emotional Cycle of Investing

7/29/25

The stock market will have ups and downs, and this can impact an investor’s emotions. Investors tend to get greedy and buy when markets are growing and get fearful and sell when markets are dropping. Buying high and selling low is not a great investing strategy.

To counteract these tendencies, investors can better understand the emotional cycle of investing, so they don’t overreact when inevitable market drops occur. Understanding can help you “stay the course”.

Umbrella Insurance

7/22/25

Umbrella insurance provides an extra layer of liability coverage beyond your existing policies, such as auto and homeowners insurance. In case of a lawsuit or a claim that exceeds your primary policy’s limits, umbrella insurance can protect your assets. In some cases, the umbrella insurance company will provide lawyers to limit (their) losses.

A $1 million umbrella policy generally costs a few hundred dollars per year. However, coverage only starts after a defined threshold. If insuring through different companies, it’s important to ensure your policy coverage reaches the point where umbrella insurance begins.

Fundamental Analysis

7/15/25

Fundamental Analysis is a method used to evaluate the intrinsic value of a security, such as a stock, bond, or commodity, by analyzing various financial and economic factors. This approach is particularly relevant to stock pickers seeking a data-driven understanding of investments.

Key components of fundamental analysis include financial statements, earnings and revenue, valuation metrics, management and governance, industry and market analysis, macroeconomic factors, and qualitative factors like reputation.

Warren Buffet is a classic fundamental analysis stock picker. He performs an independent analysis to determine if a stock is over/undervalued. Fundamental investors believe that purchasing undervalued stocks is the best way to generate portfolio returns.

Fundamental analysis contrasts with technical analysis.

Technical Analysis

7/8/25

Technical Analysis is an investment strategy that involves the evaluation of securities, typically stocks or commodities, by analyzing historical price and trading volume data. This approach relies on the belief that past price and volume patterns can provide insights into future price movements.

Key aspects of technical analysis include price charts, indicators, support and resistance levels, patterns, volume analysis, and trend analysis.

Technical analysis is often used by short-term traders and day traders who aim to profit from short-term price fluctuations. Technical analysis leads to a trading rather than long-term investing approach.

Technical analysis contrasts with fundamental analysis.

Roth IRAs

7/1/25

Roth IRAs are tax-advantaged retirement accounts commonly used for retirement savings. Unlike Traditional IRAs, Roth IRAs are funded with after-tax dollars, and qualified withdrawals are tax-free. Roth IRAs provide tax diversification and substantial financial flexibility in retirement planning. Conversions into a Roth IRA often reduce lifetime taxes for those who anticipate being in a higher tax bracket during retirement years.

Roth IRAs have relatively low contribution and income limitations but there are several workarounds including backdoor Roth IRA and mega-backdoor Roth IRA strategies.

Roth IRAs are also useful as a supplement to a 529 education savings account. Rather than risk overfunding a 529 and incurring penalties, potentially excess funds can be invested in a Roth IRA. Contributions to a Roth IRA can be withdrawn at any time for any purpose.

Modern Portfolio Theory

6/24/25

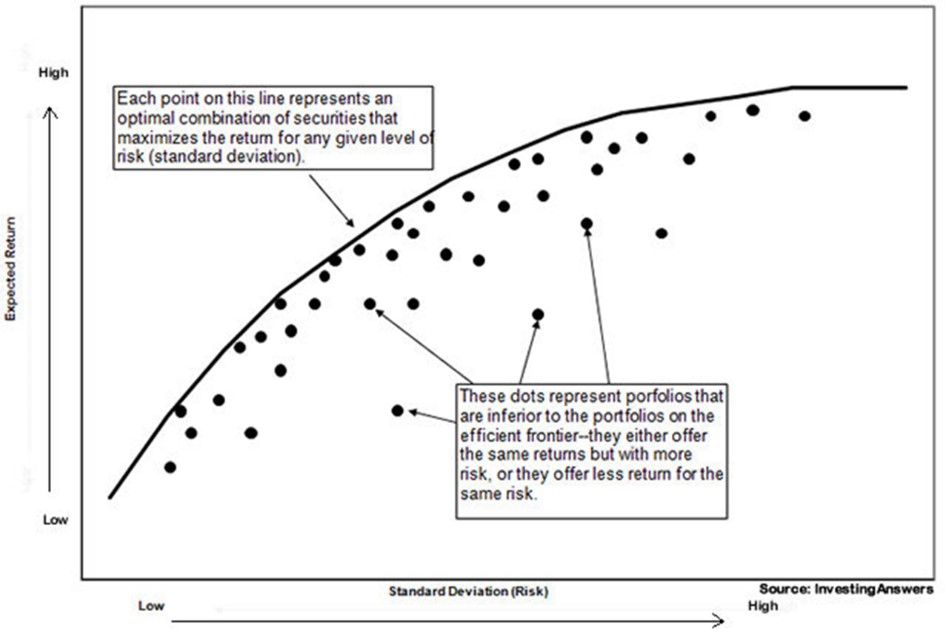

Modern portfolio theory emphasizes diversification to optimize investment portfolios. By balancing risk and return, MPT suggests constructing portfolios that maximize returns for a given level of risk or minimize risk for a desired level of return. Indexed target date funds generally fall along the efficient frontier (maximum diversification for a given return). Portfolios with individual stocks generally don’t fall along the efficient frontier.

Taxable Accounts

6/17/25

Taxable brokerage accounts are investment accounts. Unlike retirement accounts, they don’t offer tax advantages, but they provide maximum flexibility in terms of contributions and withdrawals. For many investors, taxable accounts account for a small but important portion of their overall investment portfolio.

Taxable accounts are subject to tax drag, yearly taxes on dividends that reduce overall growth relative to tax-advantaged accounts. Realized gains in excess of realized losses are subject to capital gains tax. Being mindful of the tax implications is crucial for reducing taxes and optimizing overall financial planning.

Is Managing Investments Hard?

6/10/25

Is managing your own investments hard? No. It’s actually so simple that several companies have created stand-alone programs to do it (robo-advisors). They basically recommend what’s listed in a table. It’s really that simple.

The primary value of a financial advisor is not in investment management. One should expect lower returns, not higher, if paying for investment management (fees matter, see SPIVA). The true value of a financial advisor is in providing unbiased financial advice and identifying financial opportunities and strategies that benefit the client. This has led to many advisors choosing advice-only models.

If you can use a computer, you can manage investments yourself. The time commitment is minimal (≈1 hr/yr) and Scientific Financial explains the process to all financial planning clients. We believe financial empowerment is the way of the future.

Durable Power of Attorney

6/3/25

A Durable Power of Attorney is a legal document that allows someone to make decisions on your behalf. These documents are often structured with a springing clause, so the power only becomes granted upon some pre-defined event like incapacitation. Springing clauses are typically not used in the case of caring for an older parent. A trusted child can be given legal control to handle an aging parent’s affairs on their behalf.

A durable power of attorney doesn’t have to grant all decision-making authority. It can be limited to or exclude certain aspects like real estate, stock/bond transactions, banking, business operations, legal affairs, tax issues, etc. The document may restrict the assigned from gifting away the grantor’s property (to others or themselves). Since decision making authority is powerful, it’s important to ensure the assigned person is trustworthy and proper limitations have been considered. The granted power expires at the principal’s death.

A durable power of attorney is a legal document that must be drafted by a lawyer. It’s often part of an estate documents package.

Building an Investment Portfolio

5/27/25

Building an investment portfolio isn’t nearly as complex as many assume. It’s simple if you know some underlying principles.

- Holding individual stocks reduces portfolio efficiency.

- Active fund performances resemble luck, not skill.

- Passive funds typically outperform active funds.

- Diversification reduces risk.

- The market is “efficient”. Prices adjust based on expectations.

- Lower fees mean more of your money stays invested.

From those data supported principles, it’s a logical step to utilize low-cost, broad-based, passive index funds. Bogleheads routinely tout the 3 Fund Portfolio. It’s an excellent approach – simple, low cost, and highly diversified. Combining this approach with asset location principles for tax-efficiency leads to an extremely efficient portfolio.

Unfortunately rebuilding a portfolio is more complex than starting from scratch. There may be tax consequences and required workarounds. Scientific Financial provides detailed portfolio recommendations in all financial planning engagements.

Dividend Re-Investment Plans (DRIP)

5/20/25

DRIP, or Dividend Reinvestment Plan, is a financial arrangement that allows investors to automatically reinvest the dividends they receive from a company’s stock back into additional shares of that same stock. Often the option to re-invest dividends can be selected online.

With the DRIP enabled, reinvestment happens automatically without you having to take any action. DRIPs often buy fractional shares to maximize the compounding growth of your investment over time. Typically, DRIPs have no transaction fees.

Whether to participate in a dividend reinvestment plan is a personal choice. Often younger investors choose to reinvest dividends to keep their money fully invested. Sometimes retired investors prefer to receive dividends in cash to support their lifestyle.

I Bonds

5/13/25

I Bonds are U.S. Treasury savings bonds. They are a low-risk investment option designed to protect against inflation. I Bonds offer a fixed interest rate that is combined with an inflation rate component, which is adjusted every six months based on changes in the Consumer Price Index (CPI). This means that your investment keeps pace with inflation. They can be purchased from the U.S. Treasury in electronic form up to $10k/person/year. I Bonds are considered a safe and inflation-protected addition to a diversified investment portfolio.

I Bonds aren’t designed for significant growth, but rather to hedge against inflation.

Statement of Income and Expenses

5/6/25

A statement of income and expenses is a financial report to evaluate the financial performance of a business, organization, or individual over a specific period of time, typically a month, quarter, or year. On a personal basis it shows inflows and outflows and can help you understand where your money goes. A statement of income and expense can be powerful to 1) help you meet future goals, 2) ensure your spending aligns with your values.

Auto Policy Coverage

4/29/25

Nearly all of us have auto insurance, but not all of us understand it.

Uninsured or Under-Insured covers damages in case the party responsible does not have insurance or enough insurance. It also covers hit-and-run accidents. A 2021 study by the Insurance Research council estimated 13% of US drivers are uninsured.

Collision pays for damage to your own vehicle caused by a collision, regardless of fault.

Comprehensive covers damage to your vehicle from non-collision incidents, such as theft, vandalism, hail or natural disasters.

Collision and comprehensive insurance are often dropped on older vehicles. If your current vehicle were significantly damaged, would you repair or replace? Is your insurance consistent with that answer?

Roth Ladders

4/22/25

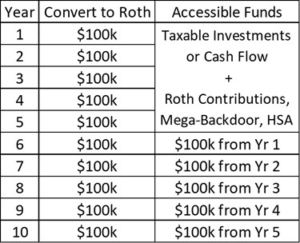

A Roth ladder is an early retirement funding technique to create future cash flows without incurring early withdrawal penalties. Pre-tax money can be converted to Roth funds by paying income taxes in the current year. However, Roth conversions can’t be accessed for 5 years after conversion. By Year 6 one can have a sustainable process to convert $100k and pay taxes on it while accessing a different $100k of tax-free money from the Roth IRA.

Planning is necessary to develop a strategy to support the first 5 years. There are many options but taxable investments, savings, current income, Roth contributions, Mega-backdoor Roth contributions and a Health Savings Account can all help. Roth ladders are a popular option for those who choose to retire at a very early age.

Restricted Stock Units

4/15/25

Restricted Stock Units (RSUs) are a common form of employee compensation, often targeting higher level employees. RSU plans are designed to increase retention by providing stock to employees. However, this “restricted” stock typically vests over several years. If the employee leaves the company, any unvested shares are forfeited.

At receipt of restricted stock, there are no tax implications since there is a risk of forfeiture. W-2 income will be recognized after shares are vested and available to the employee.

Employees with RSUs should consider portfolio risks associated with a concentrated position in a single company. It is commonly recommended to sell company stock and diversify with the proceeds.

Market Strategies Don’t Work

4/8/25

What trading strategies beat the market? None of them (today). Several trading strategies have worked in the past – dogs of the Dow, year-end or ex-dividend data trading, etc. However, once a successful trading strategy is identified, the market will adjust, and the strategy will cease working. It’s self-defeating once publicly known.

If a $1 stock movement can be expected in the future, investors will purchase that stock today, driving the price up. The price will continue to increase until it is no longer expected to produce a higher return than other options. Any known market inefficiency is quickly arbitraged in today’s computer age.

Rule of 55

4/1/25

The rule of 55 is an IRS provision that facilitates early retirement and allows for companies to offer early retirement packages. If you turn 55 during the calendar year you lose or leave your job, you can begin taking distributions from your recent employer’s retirement plan without paying the 10% early withdrawal penalty. This only applies to the recent employer’s plan – 401(k), 403(a), 403(b). This early access benefit is forfeited if funds are rolled over to an IRA. Funds in IRAs generally cannot be accessed penalty-free before age 59 ½. Although the rule of 55 is allowed by the IRS, it’s still important to verify your employer’s plan allows for these withdrawals.

Is My Inheritance Taxable?

3/25/25

Is my inheritance taxable? Inherited property is not taxable at the federal level. All federal estate taxes, if applicable, are paid by the estate of the deceased before distribution to heirs. Estate taxes are relatively rare, impacting about 0.1% of estates due to high exemption levels (2025: $13,990,000 for an individual; $27.98 million for a married couple). The probate process ensures that all creditor claims are settled before property is distributed to heirs, so any inherited property is owned outright by the heir.

Exceptions are traditional IRAs or pre-tax 401(k) retirement accounts. These previously untaxed assets are classified as “income in respect of decedent”. Withdrawals will be recognized as taxable income by the beneficiary.

Currently six states (NE, IA, KY, PA, NJ, MD) have a state level inheritance tax with varying rules.

Employee Stock Purchase Programs

3/18/25

Employee Stock Purchase Programs (ESPP) allow employees to buy company stock at discounted prices, often 15% below market value. Many of these plans utilize a lookback period that sets the purchase price to the lower price at the beginning or end of the offering period. Plans may or may not have a minimum holding period.

ESPPs can be viewed as a portion of employee compensation. They often provide valuable benefits to employees and should be strongly considered.

Dow employees not taking advantage of their ESPP can schedule a free chat with Scientific Financial. Dow’s offering is very attractive.

Behavioral Finance Biases – Herding

3/11/25

Behavioral finance bias refers to how psychological biases influence financial decisions. One common behavioral finance bias is herding. People tend to follow the masses or the “herd”. People tend to get optimistic or pessimistic about the stock market at the same time. The same can happen with individual stocks driving a stock to an unsustainable valuation. Jumping on the bandwagon often leads to longer term disappointment when markets return to balance. The herd has a tendency to get greedy and invest more as prices go up. The herd experiences fear and sells when prices fall. Buying high and selling low is not a great strategy. Generally, staying the course works better than following the latest investing trends.

Deductions vs Credits

3/4/25

Deductions reduce your taxable income, which in turn lowers your overall tax liability. Credits, on the other hand, directly reduce the amount of taxes you owe. Both deductions and credits can significantly impact your tax situation. While deductions vary based on eligible expenses, credits provide more direct tax relief.

For a 25% marginal rate, a $4 deduction would reduce tax liability by $1. A $1 credit also reduces tax liability by $1.

The Experts Aren’t Experts

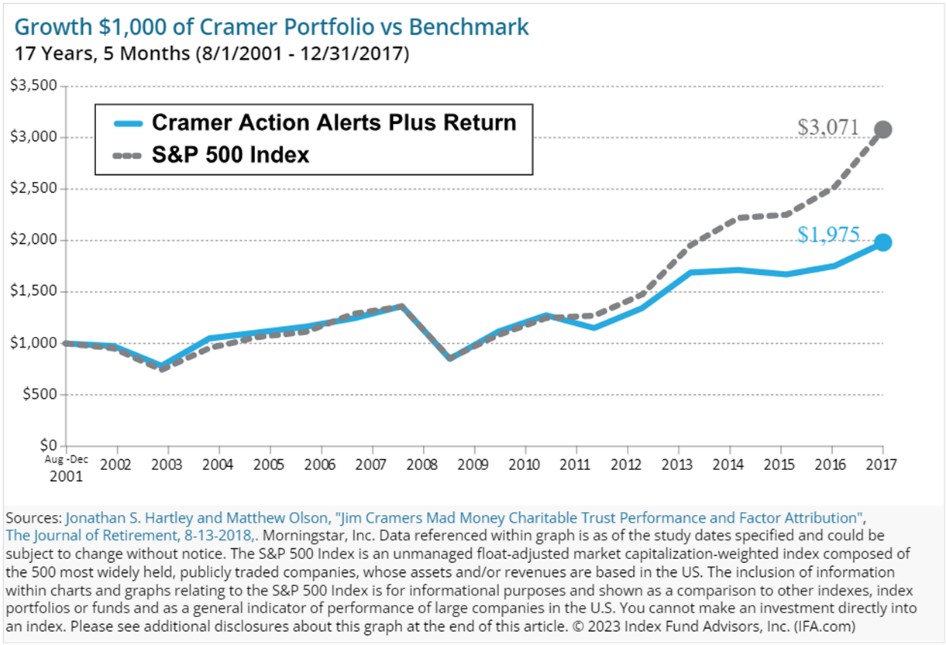

2/25/25

Do you wish you could invest like the experts on TV? I don’t. Those “experts” are just entertainers. Consider Jim Cramer – Host of CNBC’s Mad Money. A 2018 Wharton School study found his Action Alerts PLUS portfolio returned 4.1% annually vs the S&P 500’s 7.1%.

Cramer’s results were so bad that an Inverse Cramer Tracker ETF was created that “seeks to provide investments results that are opposite of recommendations by television personality Jim Cramer.” Wow!

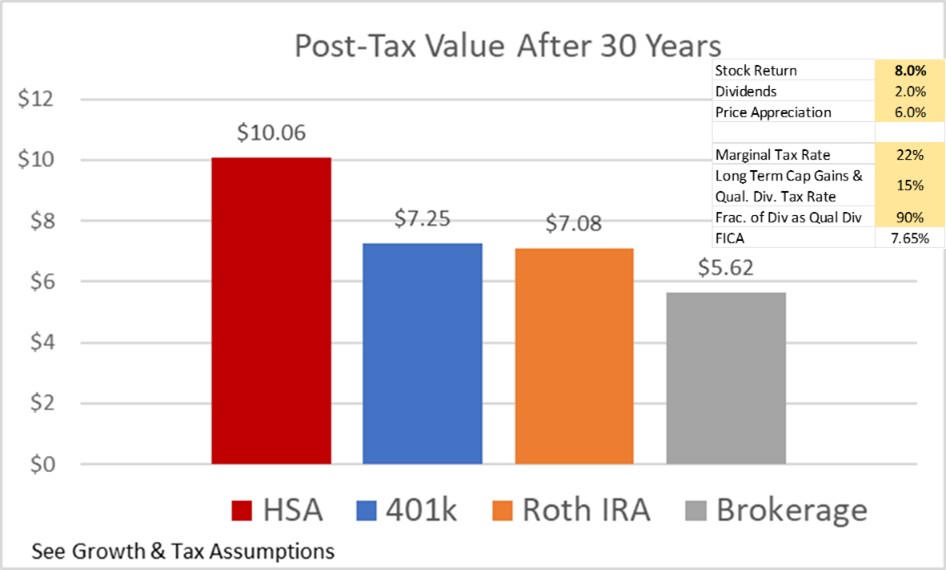

Account Tax Status Matters

2/18/25

Many investors focus on choosing the right investments but neglect choosing the right accounts. The tax treatment of an account plays a major role in maximizing returns. Below is the 30-year balance on a hypothetical $1 pre-tax investment with a yearly return of 8%.

The tax nature of a Health Savings Account leads to a dramatically larger post-tax balance vs other investment accounts. Pre-tax 401(k)s and Roth IRAs are nearly identical in their tax liability. Brokerage accounts are not tax advantaged (but provide flexibility), and those increased taxes reduce post-tax returns.

It’s not just what you invest in. It’s how you invest in it.

Options: Calls and Puts

2/11/25

Options are not appropriate for most investors. They’re essentially side bets in financial markets. Unlike investing, options are a zero-sum game – every winner is matched to a loser.

Call Option: This gives the holder the right (but not the obligation) to buy a specific asset at a predetermined price within a set time frame.

Put Option: This gives the holder the right (but not the obligation) to sell a specific asset at a predetermined price within a set time frame.

Assume an employee is granted $300k of ABC stock but must hold it for 6 months. This results in substantial portfolio risk. The employee could reduce risk by buying a put option. If ABC stock goes up, the employee will not exercise the option and can sell the appreciated stock in 6 months. If ABC stock goes down, the employee can exercise the option and sell ABC stock in 6 months at the higher pre-determined price. For the fee of purchasing the put option, the employee guaranteed they could sell ABC stock for at least the option’s predetermined price. It’s insurance, not investing.

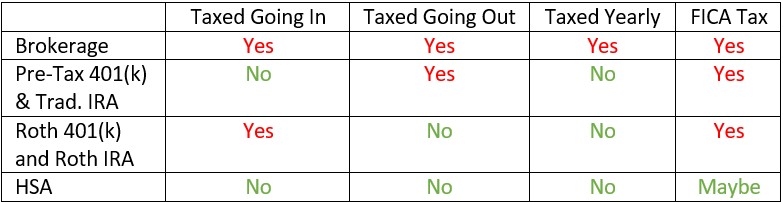

Tax Status of Investment Accounts

2/4/25

Investment accounts can have different tax status. These differences introduce strategic investment location opportunities. For example, Roth IRAs are well-suited to hold stocks since future gains are untaxed. Traditional IRAs and pre-tax 401(k) are well-suited to hold bonds since these accounts have the highest future tax liability. Roths can be favored in low-income years while pre-tax accounts may be favored in high-income years. Understanding the tax code and account tax status is the best way to reduce lifetime taxation and maximize your post-tax returns.

Many don’t consider a Health Savings Account for investment opportunities. However, when utilized as an additional retirement account it becomes the most tax-efficient account available.

Value of a Financial Advisor

1/28/25

A financial advisor can provide valuable financial guidance. They offer insights into optimizing investments, reducing taxes, managing risk, and creating tailored financial strategies. Advisors can help align financial goals with your unique circumstances, ensuring you’re aware of opportunities and potential pitfalls. While they can’t predict market outcomes, their expertise helps in making informed decisions. Engaging with a qualified advisor can lead to a clearer financial path, enhancing your ability to achieve both short-term and long-term objectives.

Terms like fee-only, fiduciary, advice-only, independent, CFP® may be important considerations in selecting a financial advisor. You can interview multiple financial advisors for free. You’re in charge!

What is a CD?

1/21/25

A Certificate of Deposit (CD) is a financial instrument where you deposit a fixed sum of money with a bank or credit union for a predetermined period, typically ranging from a few months to several years. In return, you receive a fixed interest rate that is generally higher than regular savings accounts. CDs are a low-risk, interest-bearing investment option. It’s essential to be aware of the CD’s maturity date because withdrawing funds before maturity may result in penalties. CDs may supplement the bond portion of a portfolio and provide additional diversification.

CDs are sometime used for near term, planned purchases (house down payment, college tuition, etc.) Investors can use CDs to lock in a rate and ensure they have a known amount of cash when an expense is due.

Are Gifts Taxable?

1/14/25

Are gifts taxable? Gifts received are not taxed. Gifts given are not taxed in the vast majority of cases. However, there are specific rules and limits regarding gift taxes to prevent exploitation of the estate tax system. If an individual gives a gift above the annual exclusion limit ($19,000 in 2025; $38,000 per married couple), they may need to file a gift tax return. However, gift tax is usually not owed until the lifetime gift exclusion limit is exceeded ($13.99 million per person in 2025).

Takeaway: Gifts taxes are a nonissue for most families. Gift taxes only apply to a donor who has made very large gifts.

Stock Splits

1/7/25

Stock splits are corporate actions where a company divides its existing shares into multiple new shares. It’s a strategic move, typically done to make the stock more affordable for a broader range of investors. For example, in a 2-for-1 split, each existing share is divided into two new shares, effectively halving the stock’s price.

A reverse stock split is the opposite of a regular stock split. For example, in a 1-for-5 reverse stock split, every five existing shares become one new share.

Although market responses can be fickle, value isn’t created or destroyed by stock splits. It’s just a simple mathematical maneuver to partition stock into packages of a desired size.

Treasury STRIPS

12/31/24

Treasury STRIPS, or Separate Trading of Registered Interest and Principal Securities, are secondary financial instruments. Financial institutions create STRIPS by “stripping” or separating the interest payments and principal of a Treasury note/bond and selling them as individual securities. STRIPS allow investors to purchase and trade specific components of a Treasury bond. They are typically bought at a discount and pay no periodic interest but provide a fixed return at maturity. STRIPS have a low-risk nature due to government backing of U.S Treasury notes/bonds.

Example: A 7-Year U.S. Treasury note yielding 4% has 14 semi-annual payments and a return of principle. These 15 cash flows are sold individually as STRIPS. An investor may not want the regular cash flow of a 7-Year U.S. Treasury note. That investor can purchase a STRIP to only receive the semi-annual payment due in 6.5 years.

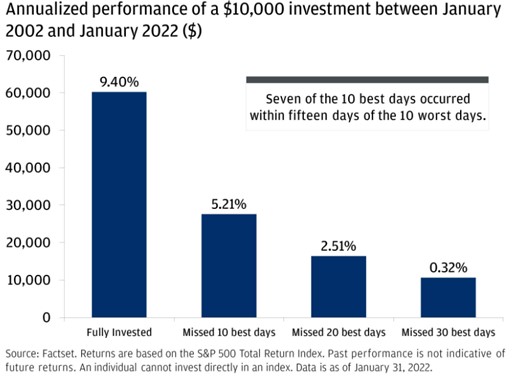

Darkest Before the Dawn

12/24/24

Markets drop and that’s scary. However, it’s generally best to stay invested. It’s often darkest before the dawn. The graphic below from Factset shows just how impactful missing the best market days can be. Many of those best market days occur soon after the scariest market days. Investors are often best served by staying the course.

Emergency Fund

12/17/24

An emergency fund is a financial safety net. It’s a savings buffer designed to cover unexpected expenses, such as medical bills, car repairs, job loss, or other unforeseen emergencies. This fund provides peace of mind and prevents the need to rely on credit cards or loans during crises. Typically, it’s recommended to have three to six months’ worth of non-discretionary living expenses saved in your emergency fund. This prudent practice safeguards your financial stability and allows you to address challenges without derailing your long-term financial plans.

Medicare

12/10/24

Medicare is a federally funded health insurance program in the United States primarily designed for individuals aged 65 and older. Original Medicare is divided into 3 different parts:

- Part A: Hospital Insurance – Covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care.

- Part B: Medical Insurance – Covers outpatient care, doctor visits, preventive services, and some home health care services.

- Part D: Optional Prescription Drug Coverage – Provides prescription drug coverage through private insurance plans.

Part A typically has no premium. Parts B and D have premiums that may vary with income. Medicare has a unique set of co-pays and other terms.

Why You Shouldn’t Pick Individual Stocks

12/3/24

Choosing individual stocks can be risky, and there are several reasons why many investors opt for other investment strategies. Those reasons include lack of diversification, market volatility, time-consuming, limited information relative to institutional investors, and emotional bias.

Nobel prize winner Harry Markowitz developed modern portfolio theory. His efficient frontier theory explains why a relatively small basket of individual stocks should be expected to have sub-optimal returns. More diversified approaches using indexes or target date funds are expected to yield higher returns for a similar risk profile.

Why Tax Loss Harvesting Isn’t as Good as It Seems

11/26/24

Tax Loss Harvesting may generate a lot of buzz, but its benefits are often exaggerated. Tax loss harvesting is a strategy used in investment management to minimize capital gains taxes by selling investments that have experienced losses.

Tax loss harvesting creates lots and lots of complexity, requiring significant time (aka cost) in properly maintaining the strategy. This may be worthwhile for multi-million-dollar taxable portfolios, but not for the vast majority of American families.

Most investors have the majority of their assets in tax-advantaged accounts (401(k), 457, Roth IRA, 529, HSA, etc.). These accounts don’t have capital gains taxes to avoid.

Tax loss harvesting primarily benefits investment managers. Once the strategy has been adopted, the investor has 2 choices: remain reliant on the advisor to manage the strategy or pay significant taxes to abandon the strategy. Think twice before adopting this strategy.

Balance Sheet

11/19/24

A balance sheet is a financial statement to assess the financial health and position of a company, organization, or individual. It provides a snapshot of the assets, liabilities, and equity at a specific point in time. Relating to personal finance, Assets – Liabilities = Net Worth.

A personal balance sheet can provide a clear understanding of your financial picture, including the value of possessions, the extent of debts, and overall net worth. Analyzing a personal balance sheet can guide financial planning, decision-making, and goal setting.

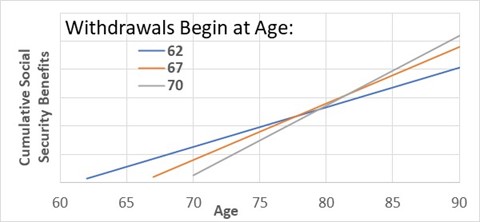

Taking Social Security at 62 vs 67 vs 70

11/12/24

Social Security is a government program that provides financial support to individuals who are retired, disabled, or survivors of deceased workers. Payments are adjusted for inflation each year and continue throughout a retiree’s lifetime.

Retirees can choose to begin withdrawals between age 62 and 70. Earlier withdrawals result in a lower payment but more lifetime payments. Later withdrawals result in higher payments but fewer lifetime payments. The breakeven points are near average life expectancies. The best option will vary by individual and is often dictated by health and financial situation.

Wills, Executor and Guardianship

11/5/24

Wills are crucial legal documents that specify how some assets and possessions will be distributed after one’s passing. Wills do not control distribution of all assets. Bank accounts, investment accounts, houses, cars, etc. may have transfer on death (TOD) titling or have beneficiary designations. These assignments supersede the will and bypass probate. Probate is the legal process through which the court validates and administers a deceased person’s will. Wills are designed to transfer other assets and the remainder of the estate.

Wills should name an executor. The executor’s role is to document all assets, handle outstanding debts/taxes, navigate the probate process and legal issues, and assist with distributing assets after probate. The executor closes all the loose ends on behalf of the deceased.

Wills are also very important to assign guardianship of minor children. It’s much better for you to choose a guardian than a court on your behalf. A court may be forced to choose the closest relative, rather than the best environment for your children.

Types of Annuities

10/29/24

Annuities are a commonly misunderstood and often overhyped financial product. Types include fixed, variable, immediate, deferred, indexed, and longevity annuities. Although annuities generally have high expenses, commissions, surrender fees, and critically important details, annuities can be a good option for some families. Unfortunately, the typical complexity and nuance in annuities is beyond the average investor’s knowledge and many make poor annuity decisions. It’s best to discuss these complex products with a knowledgeable financial advisor who won’t be compensated based on your decision.

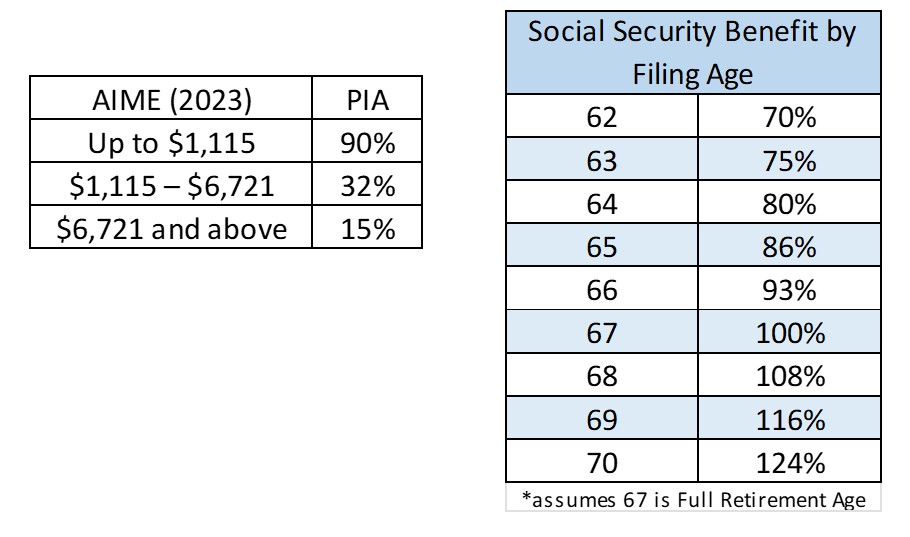

Social Security Payment Formula

10/22/24

The social security payment formula is complex but worth understanding. The Social Security Administration considers your 35 highest-earning years (inflation adjusted) to determine an average indexed monthly earning (AIME). It then applies a regressive benefit formula to determine your primary insurance amount (PIA). The PIA is the amount you’ll receive but will vary based on what age you choose to begin drawing Social Security.

There’s more nuance to the calculation but that’s the 95% summary. Some high wage earners may realize that retiring earlier may have a minimal impact on social security benefits.

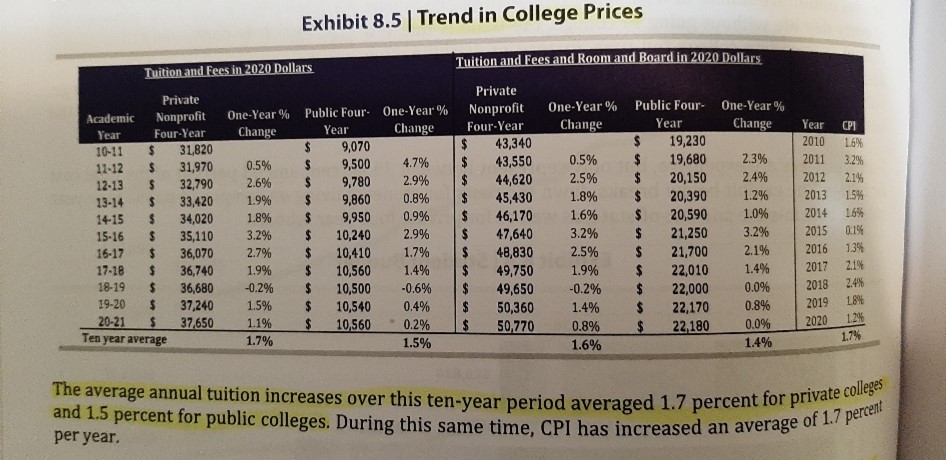

College Costs

10/15/24

It’s commonly recognized that college costs are increasing at an alarming pace. But is this true? College costs did rise rapidly in past decades (for specific reasons unlikely to repeat), but that’s not the case today. The Money Education textbook for CFP® coursework includes this startling trend. Over the last decade college prices increased in line with inflation.

FYI, I was skeptical and did some digging. My spot checks agreed with the textbook. If you’re skeptical, check historical prices yourself.

Estate Taxes

10/8/24

Estate taxes may be imposed on the transfer of assets upon someone’s death. Many assume these taxes impact typical families, but federal estate taxes only impact about 0.1% of U.S. families. 99.9% of families do not pay these taxes. Federal estate taxes only apply to asset values over the exemption limits. In 2024, the federal estate tax exemption is $13,610,000 for an individual or $25,840,000 for a married couple. In addition, there are numerous estate planning strategies to avoid or reduce estate taxes for families with assets above $27.22 million.

State estate taxes vary by state. Most states have no estate taxes (including TX & MI). Twelve states impose estate taxes with varying tax rates and exemption levels.

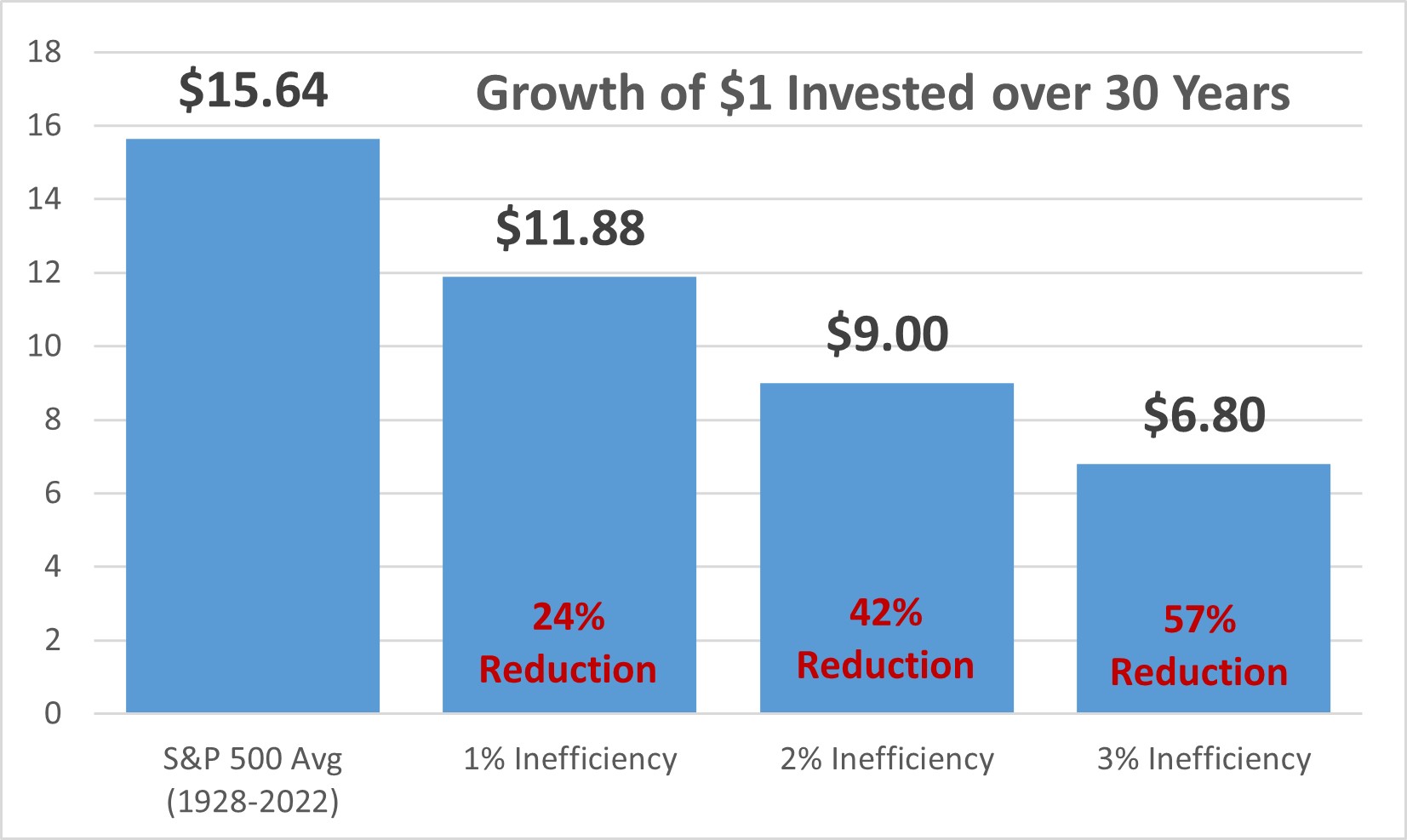

Impact of a 1% Fee

10/1/24

Recent research has shown that many investors underperform the market by 2-3% due to high fee fund selection, excessive trading, exiting to cash, etc. Many investors don’t consider a 1% fee significant, but a 1% fee historically can result in a 24% reduction over 30 years. Compounding is powerful. Inefficiencies and fees matter!

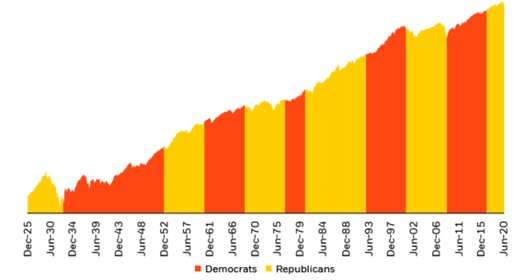

The Stock Market Doesn’t Care Who’s President

9/24/24

Some voters think that the stock market performs better under one political party than the other. Over the last 100 years the stock market has done better under Democrats, but that does not imply cause and effect. Macro-economic events play a much larger role than who sits in the White House. The stock market soared under Bill Clinton (+210%: the internet) and lost ground under George W. Bush (-40%: dot com bust, 9/11, housing crash). Barack Obama (+182%) benefited from the housing recovery, and the market has continued to grow under Donald Trump (+63%) and Joe Biden.

The stock market doesn’t seem to care who’s President.

![]()

Advantages of an Advice-Only Advisor

9/17/24

An advice-only financial advisor can offer several advantages for investors seeking guidance:

- Objective Advice

- Transparent Fees

- Flexibility

- No Product Sales Pressure

- Maintain Control over your Assets

Unlike most financial advisors, advice-only financial advisors don’t receive reduced compensation when you pay down your mortgage, buy real estate, invest in a business, avoid a particular fund or financial product, keep retirement funds in an employer plan, or spend money enjoying your life! The advice-only model allows for transparent, conflict-free advice providing you with the best advice for your situation. You also maintain 100% control of your assets.

Present Value vs Future Value

9/10/24

Present value refers to the value of an asset today or the value of a future asset discounted to today accounting for the time value of money. Future value represents the value of an investment at a specified point in the future, considering compound interest or growth.

$100 today has much higher purchasing power than $100 will have in 2050. It isn’t always apparent whether an amount of money has a high or a low purchasing power far into the future. Financial planning software, such as eMoney and Income Lab, can toggle between present and future values to help you better understand your financial plan and purchasing power.

US and International Stock

9/3/24

U.S. stocks refer to shares of companies based in the United States, while international stocks are from companies located outside the U.S. Investing in both can provide diversification benefits.

Recently U.S. stocks have outperformed international stocks, but this isn’t always the case. Financial markets are balanced. Prices in attractive markets will rise until they become unattractive. Prices in unattractive markets will drop until they become attractive. No one knows the future with certainty, and no one knows whether domestic or international stocks will outperform in the future. Most investors benefit from having a broad-based, low-cost, diversified portfolio. Inclusion of international stocks can help diversify your portfolio.

Homeowner’s Insurance

8/27/24

Homeowners insurance provides protection for your home. It offers coverage against various risks that can damage the property or lead to financial liabilities. You may think it only covers your home, but it typically also covers most personal property inside the home, liability coverage, temporary housing expenses, and medical payments.

Homeowners insurance is a tool to mitigate financial risks associated with property ownership. Lenders often require it as a condition of getting a mortgage. It’s not uncommon for policy costs to vary by insurer so it’s a good practice to shop around from time to time.

Stocks are a Good Hedge for Inflation

8/20/24

Stocks are often overlooked as a hedge against inflation. Stocks have historically outpaced inflation rates over the long term.

Let’s take a step back and consider inflation. Inflation is when the price of goods increases. Companies that sell these products receive higher revenues for the same products. Although these companies may have higher raw material costs, they’re often able to pass increased costs to the consumer. Companies typically maintain similar profit margins over the long term. Inflation typically leads to higher long-term profits for companies, and this is generally reflected in their stock price.

A Random Walk Down Wall Street

8/13/24

“A Random Walk Down Wall Street” by Burton G. Malkiel is an incredible book to teach investors exactly how investing works. It addresses historical bubbles, current philosophies, time-tested strategies, and much more. It exposes the financial industry’s BS and propaganda with data. Although not a casual read at 400+ pages of fairly technical content, I’m aware of no better book to recommend to those who want to understand the stock market and improve their investing efficiency. This book is worth its weight in gold.

Asset Allocation

8/6/24

Asset allocation involves distributing an investment portfolio among various asset classes, such as stocks, bonds, and cash, to balance risk and potential return. The goal is to create a diversified portfolio that aligns with your goals, risk tolerance, and time horizon. A proper asset allocation strategy allows you to weather market fluctuations and achieve long-term financial objectives.

ABLE Accounts

7/30/24

ABLE accounts, formally known as “Achieving a Better Life Experience” accounts, are a financial tool designed to help individuals with disabilities and their families save money for disability-related expenses. These tax-advantaged savings accounts can be used to cover costs such as education, housing, transportation, and healthcare.

ABLE accounts are similar to 529 accounts. 529s cover college expenses in a tax-advantaged way. ABLE accounts cover expenses for disabled persons in a tax-advantaged way.

Eligibility criteria and rules vary by state. Research appropriately or contact a financial advisor if ABLE accounts may benefit your family.

Alpha

7/23/24

Alpha is an investing term used to quantify investing performance. Alpha is the difference between the actual return on a portfolio and its expected return as outlined by the capital asset pricing model.

Alpha does not refer to over-performance over a benchmark since this does not consider the riskiness of the investment (Beta). Alpha is quantified on a risk-adjusted basis and is widely accepted as the proper measure of an investment’s over/under performance.

What is a Trust?

7/16/24

A trust is a legal entity that holds and manages assets on behalf of beneficiaries. It allows individuals to transfer assets to the trust, with specific instructions on how those assets should be managed and distributed. Trusts can serve various purposes, including estate planning, asset protection, and providing for loved ones. Trusts can offer benefits like avoiding probate, minimizing taxes, and controlling how assets are used in the future.

How Much Can I Contribute to Tax Advantaged Accounts?

7/9/24

How much can I contribute to tax-advantaged accounts in 2024? There are several tax-advantaged accounts including:

- 401(k): $23,000 pre-tax, but $69,000 to the entire 401(k). The difference can include after-tax contributions that can potentially be rolled to a Roth IRA. For dual income families, these values apply to each spouse individually.

- Health Savings Account: $4,150 individuals; $8,300 families. This is a great one and a high priority to fund since it can completely avoid all taxation and can typically be invested in stocks. Strategically, it’s more of a super-advantaged retirement account than a health reimbursement account.

- Roth IRA: $7,000 with potential income restrictions and workarounds

- Dependent Care Flexible Spending Account: $5,000. This is a tax-efficient way to pay for a child’s daycare.

Participation in these programs can dramatically reduce your taxes. Some allow larger contributions for those aged 50+.

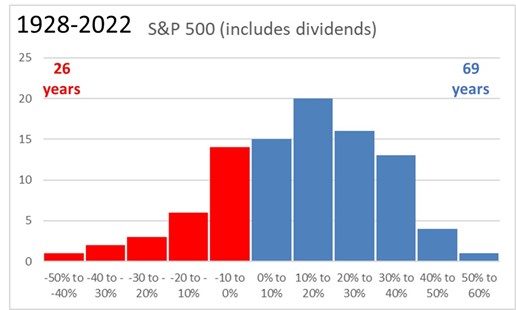

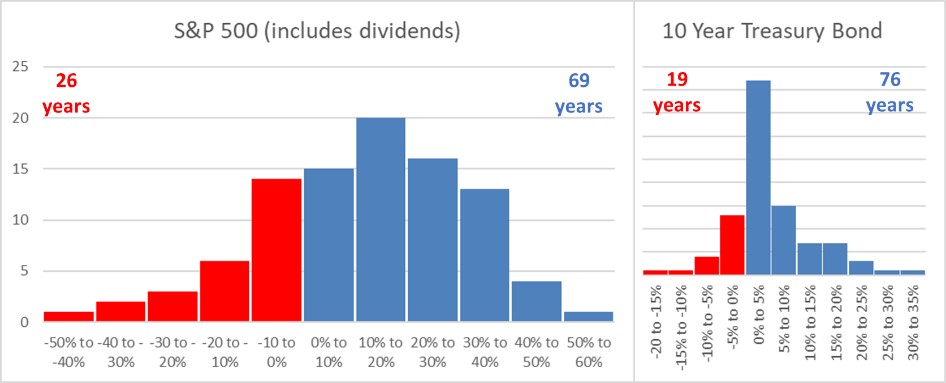

Historical Market Returns

7/2/24

Historical market returns are important to ensure investors have reasonable expectations of the future. The S&P 500 (a common gauge of the US stock market) returned an average compounded return of 9.6% from 1928 through 2022, including dividends. However, stock returns can vary dramatically from one year to the next. The plot below shows the frequency of returns. The S&P 500 has had approximately 3 positive years for every down year.

Recency Bias

6/25/24

Behavioral finance bias refers to how psychological biases influence financial decisions. One common behavioral finance bias is recency bias. If a particular stock (consider NVIDIA or meme stocks) has been performing well over the last few weeks or months, someone affected by recency bias might assume that the trend will continue and make investment decisions accordingly, without taking into account other relevant factors. To counter recency bias, it’s important to adopt a more comprehensive and balanced approach to decision-making. It’s best to consider historical data, long-term trends, and fundamental factors that drive financial markets, rather than being swayed solely by recent trends.

Beta

6/18/24

Beta is a measure of a stock or investment portfolio’s sensitivity to market movements. It helps assess the investment’s risk in relation to the broader market.

Beta is expressed as a numeric value. A beta of 1 indicates that the investment tends to move in line with the market. A beta greater than 1 suggests the investment is more volatile than the market, while a beta less than 1 implies lower volatility. If a stock has a beta of 1.2, it’s expected to be 20% more volatile than the market. Conversely, a stock with a beta of 0.8 should be 20% less volatile. High-beta stocks are riskier but may offer higher returns, while low-beta stocks are less risky but may have lower returns.

Beta has limitations, as it only considers historical price movements and doesn’t capture all types of risk, such as company-specific events.

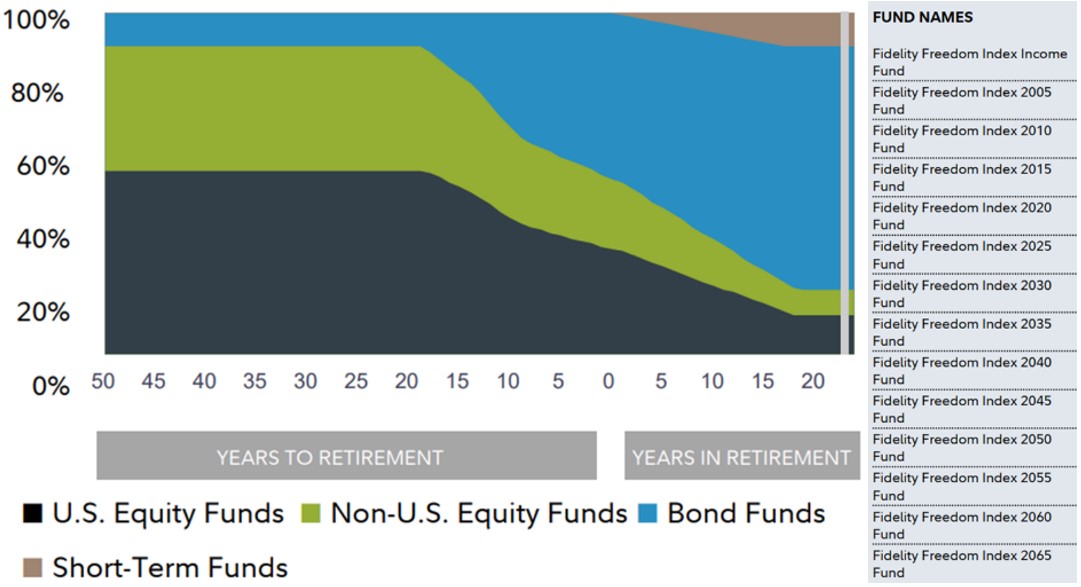

Target Date Funds

6/11/24

Target date funds have become very popular in retirement plans, and rightfully so. They often provide maximum diversification and convenience. Investors can simply choose the one with a name closest to their expected retirement date and obtain an entire investment portfolio in a single fund.

While target date funds have drawbacks, particularly around tax efficiency, they provide a solid portfolio for a typical investor. Fund design varies among the brokerages, but they typically have common qualities: use of the broadest, low-cost funds; proportional US/international stock exposure; high stock allocation in early years shifting to a more conservative portfolio over time.

Auto Policy Coverage

6/4/24

Nearly all of us have auto insurance, but not all of us understand it. Liability covers costs if you’re responsible for an accident, including medical bills and property damage for the other party. You may be responsible for damage beyond these limits.

A split policy may have 3 numbers: 30k/60k/25k (Texas min coverage)

- $30k of coverage for injuries per person

- $60k of coverage for injuries per accident

- $25k of coverage for property damage

A combined policy has 1 number which combines all bodily injury and property damage.

Consider the cost of medical treatment and the costs of new vehicles today. Then decide whether your liability coverage is appropriate.

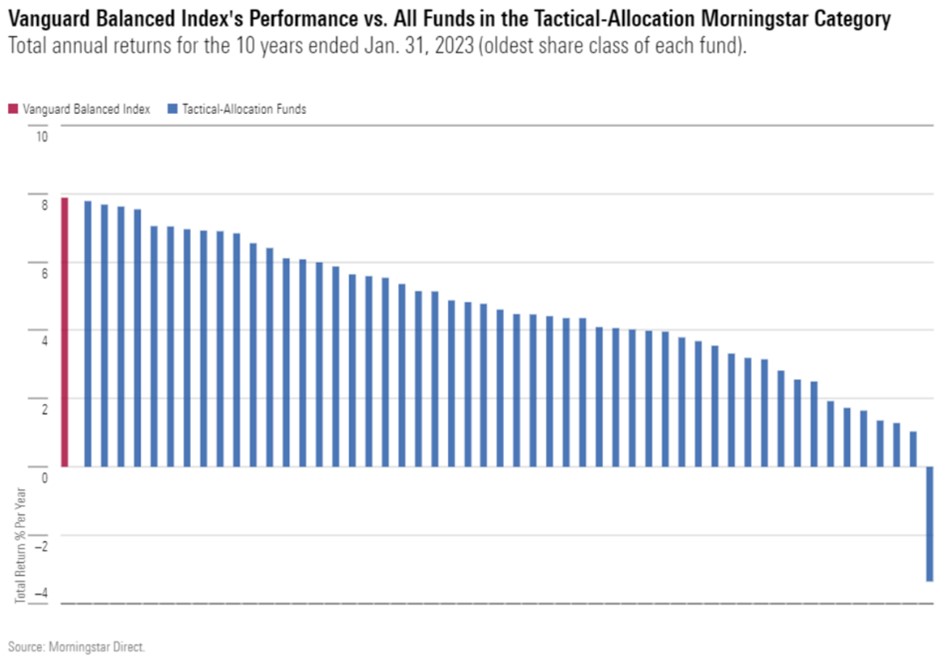

Tactical Asset Allocation

5/28/24